I’ve been an accountant for over 20 years and have worked primarily with physicians, dentists and other professionals for most of my career. Over the years, incorporation is the subject I’ve been asked most about.

- Should I incorporate my medical practice now?

- How do I incorporate?

- How does a medical corporation help me?

The questions are almost endless. And this blog post would be endless if I tried to address all aspects of incorporation. For this post, I will provide an introduction to incorporation. In the coming months I’ll expand on this basic information and show why most physicians should be incorporated.

What is Incorporation?

Incorporation is the creation of a legal entity called a corporation, also known as a company. A company is a separate legal entity that has many of the powers of an individual. It can earn income, acquire assets, enter into contracts, pay taxes, etc. When a physician incorporates, the medical corporation will carry on the business of the doctor’s medical practice.

Why Incorporate a Medical Practice?

There are many reasons for a physician to incorporate.

Income Tax Deferral

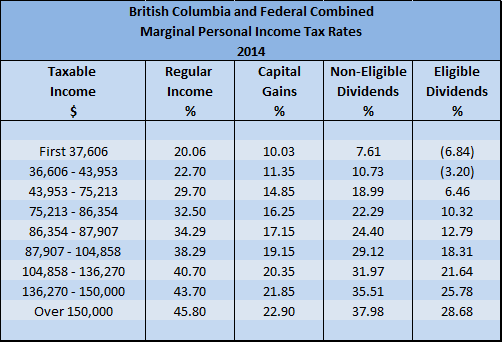

In British Columbia, personal tax on regular income between $136,000 and $150,000 will be taxed at 43.7% in 2014, and income over $150,000 will be taxed at 45.8%.

Alternatively, in a private corporation, the first $500,000 of business income is only taxed at 13.5%, and the remainder at 26%.

A doctor can defer tax of up to 32% on income in excess of $150,000 by using a medical corporation if funds are left in the company.

This deferral helps the company purchase assets, repay debt, and accumulate savings. The company has paid less tax and has more funds available for other uses.

This income tax reduction is only a deferral, and additional tax must still be paid when the doctor withdraws the funds from the company. However, with proper planning the additional tax can be minimized or even eliminated.

Income Splitting

Canada uses a graduated income tax rate system where income at different levels is taxed at different rates.

Income splitting is shifting income from a high tax rate individual to lower tax rate individuals. Two people earning $100,000 each will pay $18,000 less tax combined than one person earning $200,000.

Unincorporated doctors can split income with family members by paying them a salary. However, an expense must be reasonable to be deducted from business income. A salary of $50,000 to a spouse or other relative who has little involvement with the medical practice would probably not be considered reasonable. If disallowed, the physician does not get a deduction and the relative still pays tax on the salary – instead of reducing tax, there is double tax.

A medical corporation can also split income by paying salaries, but the deduction of salaries by a company is still limited by reasonability.

The advantage that a medical corporation has over an unincorporated physician is that it can also pay dividends to the shareholding physician and family members. Dividends are paid from the after-tax income of a company and are not subject to a reasonability limit for income tax purposes. Dividend income is taxed personally at a lower rate than regular income to take into account that some tax has already been paid by the corporation.

Income splitting is maximized when all family members are in the same tax bracket. Unless family members are very active in the practice, this can only be achieved with a medical corporation and dividends.

Cheaper Non-Deductibility

Certain expenses such as 50% of meals and entertainment, club dues, and life insurance premiums are not deductible for tax purposes. The cost of a non-deductible expense is cheaper in a medical corporation because the company is taxed at a lower rate than the doctor. A doctor in the highest tax bracket must earn $9,225 personally to pay a $5,000 life insurance premium (Income of $9,225 less tax of $4,225 at 45.8% is $5,000) . A medical corporation only has to earn $5,780 to pay the same premium (income of $5,780 less tax of $780 at 13.5% is $5,000).

Tax-Free Sale of Shares

A significant benefit of incorporating a business is that the first $800,000 of capital gains on the sale of qualifying shares may be tax-free under the Lifetime Capital Gains Exemption. Unfortunately, unlike other professionals such as lawyers, dentists and optometrists, physicians are not usually able to take advantage of the capital gains deduction because medical practices in BC have limited value. There may be an opportunity to use the capital gains deduction where the company owns the medical office.

Limited Liability

A company is a legal entity that is separate and distinct from its shareholders. Shareholders are not liable for debts and actions of the company. At most, they risk the loss of their investment in the company. However, legislation in BC specifically states that incorporation of a medical practice will not shield a physician from liability for professional negligence.

A medical corporation can still protect personal assets from liability for leases, non-guaranteed loans and other creditor claims against the practice. Corporate investment assets can be shielded through use of a holding company.

Other Tax Advantages

There are several tax saving strategies that require a corporation including Private Health Services Plans (PHSP), Individual Pension Plans (IPP), and death benefits. These benefits are beyond the scope of this article and will be addressed separately in the future.

Psychological

Incorporating a medical practice can have a positive effect on spending habits. When not incorporated, medical practice income is deposited into personal bank accounts which are easy to access.

When a company earns the income, it is easier to view the money as belonging to someone else. Physicians are more aware of how they are spending when they have to subsequently take the funds out of the company.

Why Not Incorporate?

Incorporation is not without some drawbacks:

Complexity

Incorporation adds an extra layer of complexity to a physician’s financial affairs. A company must maintain separate accounting records, file a separate tax return, and file T5 slips for dividends. More planning is required to transfer funds from the medical practice for personal use.

It may seem daunting at first, but over time the operation of the company becomes routine.

Financial Costs

The added complexity of incorporation is more expensive. There will be legal and accounting fees for both the set-up and ongoing operation of the company. However, the financial benefits of incorporation are far greater than the added costs.

Risk of Changes in Laws

Nothing is certain in life except death and taxes. But the way our taxes are determined is always subject to change. A medical corporation is very effective for reducing and deferring income taxes based on the rates and rules in effect today. Who can say this will still be the case 20 years from now?…but who can say it won’t?

When to Incorporate?

Most physicians should and will incorporate. But it is not always advantageous. Incorporation is best for physicians with sufficient income who can use the company to save for retirement or who can split income with family members.

What is the Incorporation Process?

Incorporating a medical practice includes the following steps:

- Name reservation with the BC Corporate Registry.

- Preparation of incorporation agreement, articles of incorporation and determination of shareholders.

- Application to the College of Physicians and Surgeons for approval to incorporate.

- Filing of Incorporation Application with BC Corporate Registry.

- Submission of incorporation documents to college for medical permit.

- Opening of bank account and paying for shares.

After incorporation, other administrative start-up tasks include registration with tax authorities, notification to MSP and other revenue sources that the practice is incorporated, notification to insurance providers, etc.

What Next?

This post is a simple introduction to medical corporations. Check the blog on a regular basis for future posts with more detailed explanations on this topic. You can also follow the blog by email for notification of updates.

If incorporation is something you are interested in, please contact me for more information or a consultation.

![]()

Excellent article John,

An additional strategy for medical practitioners would be to hold shares of the professional corporation by using a holding company. Basically the practitioner and their family members would become shareholders of the holding company. The professional corporation would then provide loans to the holding company at the Canada Revenue Agency’s prescribed rate of interest of 2%. The holding company then invests the loan money into income producing assets (stocks, bonds, real estate).

This not only allows income splitting amongst family members, but also provides creditor protection for the corporation by transferring excess funds to the holding corporation.

I don’t usually use holding companies with medical professional corporations unless real estate or other business ventures are involved. Coverage through CMPA protects the assets from malpractice claims, and other creditors are usually a minor concern. I find that holding companies for medical professionals, although great for us accountants as another fee source, are usually unnecessary. I’m not saying that they shouldn’t be used – each situation is unique and there may be circumstances that warrant the extra protection.

Just a quick question, someone mentioned that the medical/dental professional corporation has to use a Licensed Public Accountant to get their year-end done. is that right? is there any mandatory requirement by the association that the financial statements has to be prepared/audited by a Licensed Public Accountant?

There is no requirement that a designated accountant prepare the financial statements. If the company has bank debt and the bank is requiring proper accountant prepared financial statements, you will need an accountant, but otherwise anyone can prepare the statements / year end.

Year end financials have to be done for the corporate tax return, so you may want to use an accountant to make sure you are getting all the deductions you are entitled to, and getting good tax and financial planning.

Thanks for making this complex topic simple. I have a question. Once you have run the PC for a number of years and its time to close shop and retire, what happens next and how do you get the money out of the corporation before it is wind down completely. Is there a tax efficient way to do this. Also if one has bought real estate from the income within the corporation, once the company closes do I have to sell the real estate or can it be transferred under my name or my spouse/children.

There is no requirement for the company to end when you stop practicing. The company continues on as a holding company until the assets are depleted.

The main idea behind using the company to save is that the accumulated assets of the company are eventually taken out as dividends when you stop working and your income is lower.

Hi John,

Does a BC medical corporation have to be linked in any way to WorkSafe BC?

Thanks,

DD

A BC medical corporation has to be registered with Worksafe BC – required to pay Worksafe premiums on wages paid to employees and dividends paid to active shareholders

My wife is a Nurse Practitioner and works under a self-employed contract for a family healthcare clinic in Ontario. I am a Professional Enginer and have a corporation registered in Ontario. Can my wife’s business (medical services) be added to the existing corporation. What changes need to be made in the incorporation documents and how her income from medical service, which is HST exempt, can be added to the existing corporation income?

Thank you for your help,

The Nurse Practitioner business can’t be added to the existing engineering company. Under the Regulated Health Professions Act (Ontario), a regulated health profession requires a certificate of authorization. One of the conditions for obtaining the certificate of authorization is that the articles of the corporation state that the corporation cannot carry on a business other than the practice of the profession governed by the College and related activities. Here is a link to the College of Nurses of Ontario http://www.cno.org/what-is-cno/regulation-and-legislation/legislation-governing-nursing/

Thank you very much for this excellent post, after reading your article I finally understand this whole subject a lot better after many years of struggling with it.

I am a physician in a group practice with 4 other doctors, and we share an office where we each have either 1 or 2 examining rooms. There is no space however, for any of us to have a proper desk/workstation where we can do dictations, go over paperwork or complete reports, or even have a private telephone. I have been doing most of those tasks in my residence where I use a room as a home office, however this has become inconvenient due to various factors including distance between my home and office, lack of adequate space, etc. I am looking to purchase a small strata condo in a location next to my office building so that I can have a place close to my work which I can use exclusively as a home office and also where I can stay when I am on call so that I can be close to the hospital. Can I purchase this property with my medical corporation, as the function of this property will be for my work as a physician? Or does it have to be purchased with a holding company?

Thanks very much

As the strata unit will be used mainly for business, it can be purchased by your medical corporation, and all of the related expenses (strata fees, utilities, property taxes, etc.) can be deducted. No need to purchase it through a holding company as it will be used in the business. The company should charge you rent for any personal use of the property (relatives or friends staying in it). I would argue that your staying in the unit while on-call would be business use.

Hi John,

I have another somewhat related question which I would like to ask you please, can the medical corporation be used to invest in things like stocks and investment properties even if those items are not necessarily related to the practice of medicine? I have heard opposite views regarding this, and know of some physicians who have bought investment properties and stocks with their medical corporations. Their argument is that these investments are not for personal use but are to make money for the corporation. I have also heard that Revenue Canada frowns upon accumulating excessive amounts of cash within a medical corporation, and so that may be another reason to put the money that is in the corporation towards business investments.

Thank you very much,

Definitely. A medical practice cannot operate any type of business other than the practice of medicine, but it can hold investments – they are not considered a business as they are passive in nature. Stocks, bonds, rental properties – all can be held (at least in BC).

Accumulation of cash is not a problem – a few hundred thousand dollars of cash in a bank account, or stocks, or properties – it is all the same.

The ability to claim the small business deduction can be impaired if the value of the company gets too high, but that is when in the $10 million range – not many medical corps reach that amount.

Hi John

Thanks for sharing your knowledge. I am hoping you might provide some details as to what is involved, or if it is possible to add second generation MDs to an existing Med Prof corp..

It is understood that the 500 k would be shared.. It seems that year end must be Dec 31.?

Just wondering if the retained earnings in the corp can be assumed by the second generation for estate planning?, If the second generation wants the freedom to move to the US or another province could they leave their earnings in the original Med Corp as long as it remains active?…What are the possibilities to transfer retained earnings from one province to another..

Ps We all dream of moving to BC.(not Vancouver too many $$$ ) ..

most sincerely e

I am so sorry for the delay in publishing this response. I originally wrote the response back in September, but apparently it was never published. Possibly user error, but I blame the software.

Lots of questions, which I can’t answer simply without asking a lot of questions myself. You will definitely need to consult with a tax advisor about your specific situation.

Some general comments:

I wouldn’t recommend multiple physicians practicing through the same medical corporation unless there is no way around it – complicates the planning, especially with the new rules introduced by the budget earlier this year.

A medical corporation is not required to have a December 31 year end, unless it is in a partnership.

The 2nd generation cannot “assume the retained earnings” unless they are already shareholders. Even then, it depends on the rights and restrictions of the various issued shares. Often the 2nd generation shareholders have special restricted shares that do not have access to the value of the company.

A medical corporation cannot operate in multiple provinces at the same time. A new company can be incorporated in the new province, or the existing corporation can be transferred / continued to the new province. Sometimes a new company is created for the new province, and the old company becomes a holding company for the investments / assets that have already accumulated.

Thanks for the article. I have a question on multi-provinvial jurisdiction. I was considering setting up a CBCA corp so that two MD’s (Ontario and BC) could flow their earnings through the company. Are there any issues in getting provincial medical board approval for such a set-up?

I am so sorry for the delay in publishing this response. I originally wrote the response back in September, but apparently it was never published.

A CBCA corp won’t qualify for licensing as a medical professional corporation. Most provinces require that a medical professional corporation be incorporated in (or continued into) that jurisdiction. I don’t believe that any medical corporation incorporated in one province is eligible for licensing in another province (without continuing to the other province). The only solution is multiple corporations, one for each jurisdiction.

For example, the College of Physicians and Surgeons of Ontario specifically states that a CBCA corp will not qualify as a medical corporation in Ontario

http://www.cpso.on.ca/CPSO-Members/Incorporation-Issuance-and-Renewal

Hi John,

Considering my spouse is a professional engineer with his own corporation making in the range of $200k/year and I’m a new MD starting my career this summer; at witch stage should I incorporate ? I estimate that for the first 2-3 years I won’t break the $100-150k/ year and I see no benefit of income splitting.

Also, if I don’t incorporate how do I run my practice ?

You don’t need to be incorporated to run your practice – can be operated as a sole-proprietorship (self-employed).

If income splitting is not currently an option (high income spouse, high income parents and high income grandparents), incorporation is still useful if you can set aside funds for investing. However, if your husband already has a corporation, the investing can be done there for the time being. No point in paying two sets of legal and accounting fees which eats into the investment return.

At your forecast level of income, it won’t be worthwhile to incorporate for awhile unless you are looking at purchasing a strata unit or building for a clinic in the near future.

Hi John,

I really appreciate your answer but you’ve also raised another one for me. You mentioned parents and grandparents. In our case, both families have virtually little or no income but they are abroad in a country to whom Canada has a convention regarding the avoidance of double taxation. Will that income splitting with parents work?

Income splitting with non-resident parents / grandparents is a bit more complicated but is possible – depending on the countries involved.

In the case of non-resident shareholders, tax is withheld on any dividends declared to non-residents. The general rate of withholding tax is 25%, but the rate may be lower depending on the terms of the tax treaty between Canada and the country of residence. For example, the rate is reduced to 15% for residents of the UK, US and China among many others.

In most cases the recipient reports the income on their tax return in their country, and can claim a foreign tax credit for the tax withheld by Canada which often fully offsets the income tax.

The decision to implement income splitting with parents and grandparents, whether resident or not, needs to take into consideration the impact of the additional income on any retirement or other benefits they may currently be receiving.

Thanks for a great post!

I have a question about when to withdraw money from the corporation. For example if I am making 200k/year and take 100k from the corporation to pay my personal salary and leave 100k in the corporation which to my understanding would get taxed at a lower rate (around 15%).

1) What would be the most tax-efficient way to withdraw some of the money from the incorporation, or will I be double-taxed?

2) Is it possible to otherwise leave the money in the corporation and pay things such as car expenses, repaying medical student loans? (What kind of things can be written off or paid by the corporation rather than my salary?)

Thank You!

You won’t get double taxed on withdrawing funds from the company. If it comes out as salary, the company gets a deduction. If it comes out as a dividend, you pay a lower tax rate on the income than you would on a salary as the tax system takes into consideration that tax has already been paid at the corporate level.

The most tax efficient way of taking funds out is through income splitting with lower income family members – spreading the tax burden among others to use up their lower tax brackets instead of all being taxed to you.

If income splitting isn’t available, need to monitor what/when funds are taken out and the relevant tax brackets. For example, may not be worthwhile to take all money out in a year to pay off student loans. The higher personal tax paid on the funds used to payout the loan may end up more than the interest saved as compared to taking the funds out over 2 – 3 years at a lower personal tax rate.

The company can pay for expenses used to earn business income, investments, etc… There are certain expenses that can be switched to company on a tax advantaged basis (life insurance, medical expenses). Personal expenses such as student loan repayments will always be considered personal – if company pays your student loan, it is income to you.